Award-winning PDF software

About form 8288-b, application for withholding certificate - internal

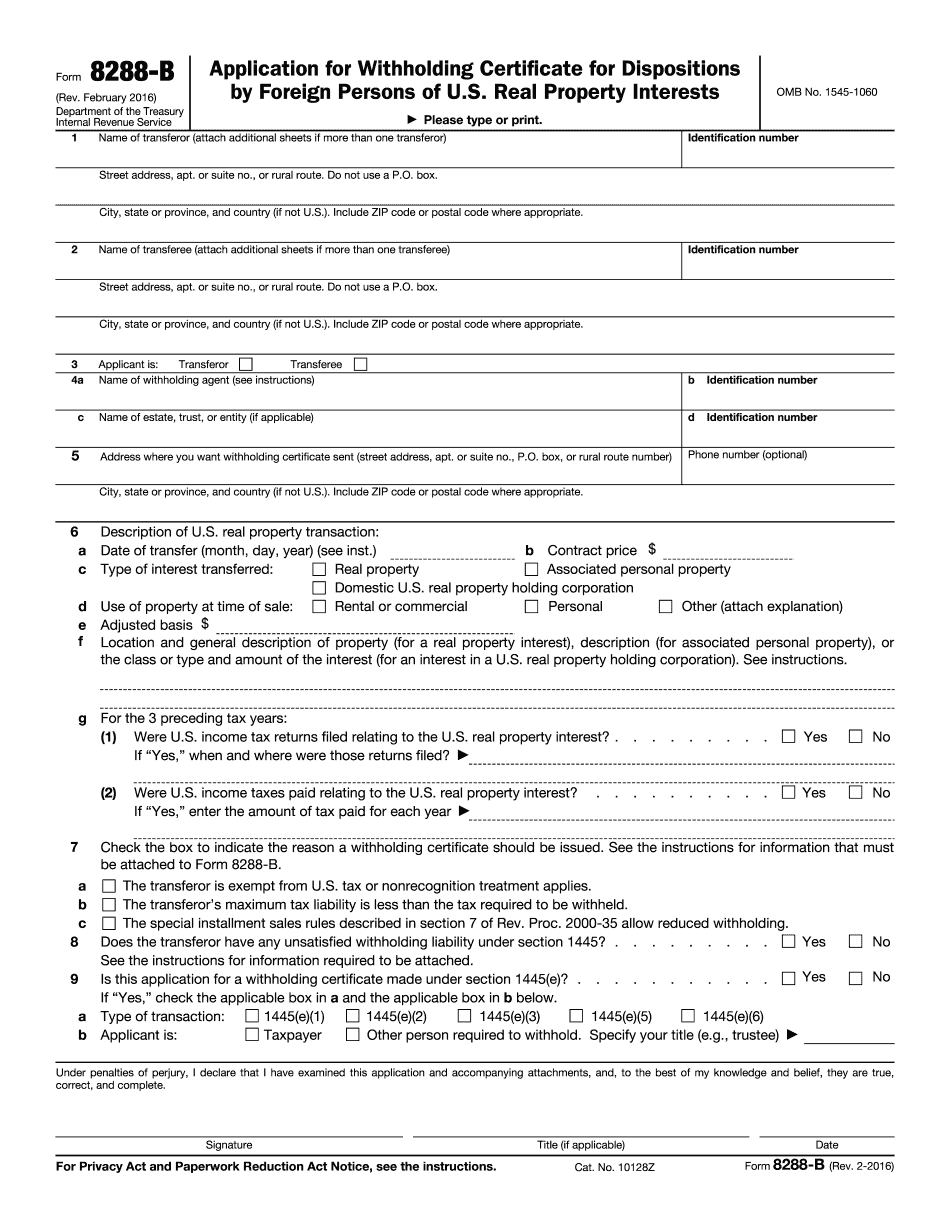

See Publication 1036, Income Tax Withholding for more information. The 8288-B forms provide specific instructions for determining if any foreign entity is required to withhold tax on property sales. See Publication 551, Foreign Tax Credit and Foreign Tax Billing, for more information. Section 960 of the 2010 Code gives foreign persons holding real property a 100% exclusion from tax on the sale or exchange of such property held for more than 12 months. For more information on sales and exchanges of real property by real property holding entities, see Publication 542, Foreign Tax Credit, or Treasury Regulations section, Imposition of a 100% Exclusion From Tax : Real Property Holding Entity. The Form 8288-B is not tax information, and it does not substitute for a tax return, or tax return information. For additional information, please contact the Forms & Publications Division, Telephone:, or at tel .

form 8288-b (rev. february 2016) - internal revenue service

Filing with the Tax Collector by: 1) A foreign firm that has a qualifying real property interest in a real property interest, such as: (1) an RIO; (2) a nonzero; or (3) a qualified partnership interest; (2) an individual that is actively conducting a trade or business in the United States, as long as the individual does not have an RIO with more than five (5) qualified persons; and (3) a corporation having its principal place of business in the United States; (3) a qualifying United States person with respect to such interest; or (4) a corporation having its principal place of business in a foreign country or the United States in which its tax residency requirements are substantially the same as those in the United States; (B) File the Form 8288-B with the Tax Collector by filing Form 8288-B. Reporting for Firms With Interests in Foreign Real Property: (1) General Rule for Reporting Interests in Foreign Real Property..

Foreign investors in u.s. real property may reduce firpta

If you are not sure how much federal income tax you owe, you can check your W-2 tax statements here. In this example, I calculated my annual withholding tax liability at a 200,000 annual income. You then have three options: If you wish to file a Notice of Federal Tax Lien on the foreign-owned investment, do so no later than three years from the date the amount of your foreign-owned investment became taxable to you. If you did not file a tax return for the foreign-owned investment, you may not be able to use this alternative; however, you should consult with a tax attorney to learn if the foreign financial institution cannot use the Notice of Federal Tax Lien on the foreign-owned investment as evidence of tax deficiency and, if so, what form of relief you may be able to seek. If you file a tax return for the foreign-owned investment, the Treasury.

Refunds of the excess withholding tax/ 8288-b withholding

There's a way around this. There is a “good faith” exemption from withholding tax on the sale of residential real estate. So, you could be buying a new home and selling your old one to a non-US buyer for only tax. Now you may be thinking “surely US sellers have to pay the tax.” There is actually a very good explanation. And it explains why the exemption could allow for US buyers to get away with paying a higher price per square foot in their home. Here's the IRS explanation of why the non-US residents can avoid withholding tax on the sale of their homes: The exemption applies to real estate sold within the United States and to foreign real estate that is not subject to the United States' real property income tax. Real estate sells through multiple owners and is not held by one owner for the.

Best practices for a successful firpta withholding application by

This is one of the reasons why it is important that all of my clients submit their Form 5320 tax forms along with ALL SALES OF US RPI to avoid potential problems. -The IRS has recently announced that all Form 8288-Bs relating to SALES OF US RPI will be accepted and processed without question (as they should be). You may need to submit another form of US tax documentation for this transaction since Form 5320 documents are not accepted. Once this is confirmed, your transaction will only take a short time to be processed. This should be less than 24 hours in all cases.