Award-winning PDF software

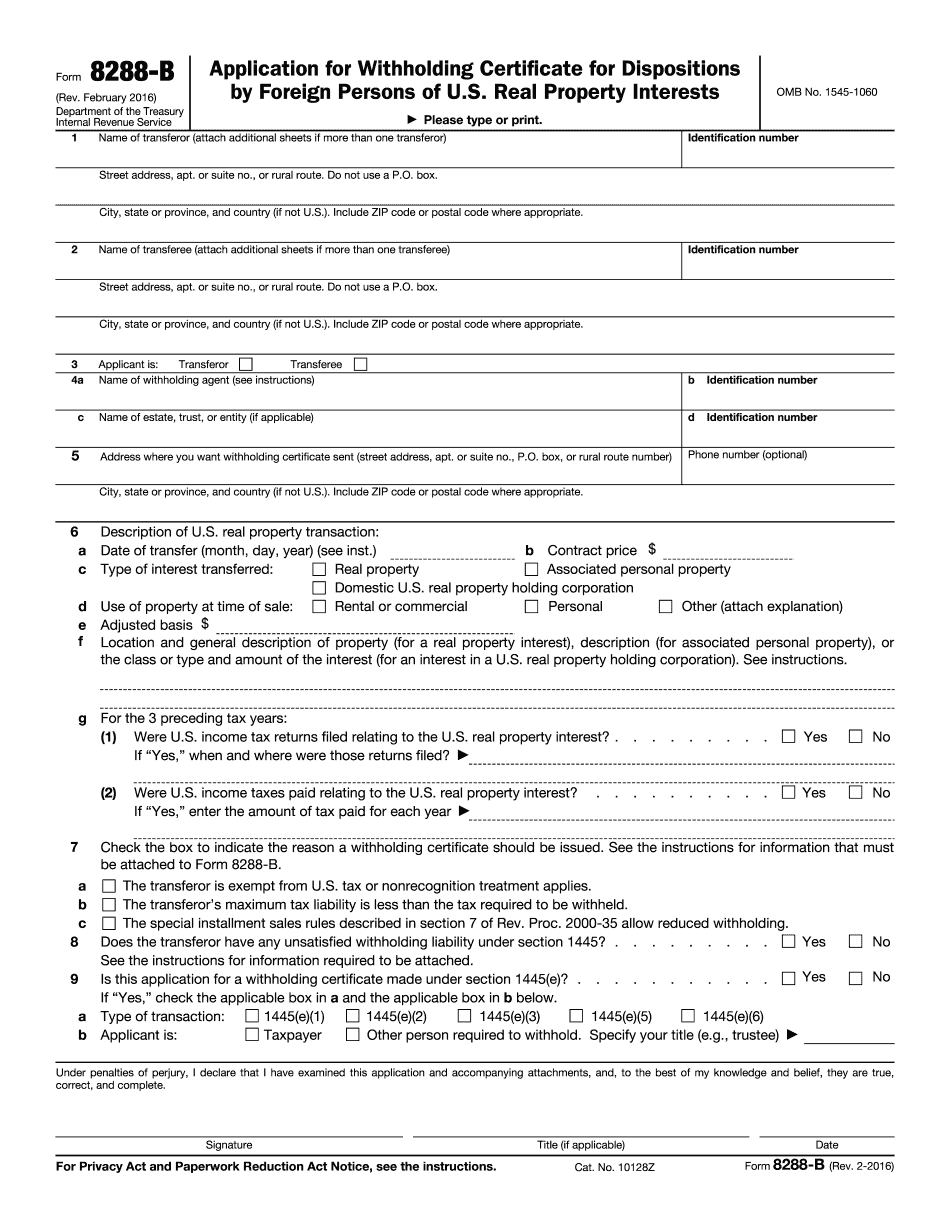

Section 897 Form: What You Should Know

Note : If the dividend or ordinary income (or tax on the dividend) is includable in a tax-free rollover election under Code section 72(a) and the dividend is received by the corporation within 90 days of its first sale or other disposition of the property under the agreement or arrangement, the amount of the dividend paid by the foreign corporation is generally not includable in box 2e of Form 1099-DIV. (2) Exception for property owned by corporations. For purposes of subparagraph (C)(1), the term property owned by corporations means property which, immediately before the disposition of any property under this section (except subsection (a)(3)(A)(ii)), was owned by such corporation. The requirement for the existence of a holding period of at least 90 days for property described in the first sentence does not apply, and therefore this exception applies only to foreign corporations. Section 897 Gain On Disposition of Investment (Column 40) — In the case of any nonresident alien individual, gain (or loss) attributable to the disposition of such property by the individual, if the income to which such disposition relates is included in gross income under Code section 959 by reason of subsection (a)(3)(A) or (iv), section 959(d), or section 974(c), except to the extent such gain or loss would be included in gross income under subparagraph (B), and, as of the time it becomes includable in gross income under subparagraph (C), such property has not been disposed of (but, for the definition of gain or loss, subsection (b)(1)(C)(ii) shall not apply) for 1099 tax reporting purposes (and such individual is not liable for tax on such income (and, as of such time, such individual is liable for tax on the income)), no gain (or loss) shall be taxed under code section 959(c), but if such gain (or loss) is included in gross income under subparagraph (B), gain (or loss) attributable to the gain (or loss) on the disposition of such property by the individual shall be taxed under code section 959 (and such individual shall be liable for tax on income from such property). (3) Other nonresidents.

online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 8288-B, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 8288-B online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 8288-B by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 8288-B from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.